How Credit Card Processing Works “Infographic”

A step-by-step explanation

Credit card processing allows you to accept different types of payment. As a business owner or manager, it’s beneficial to understand how credit card processing works.

Who is involved in credit card payment processing?

- A customer/cardholder obtains a credit or debit card from an issuing bank and uses the card to pay for goods or services.

- A merchant is any type of business that accepts credit or debit card payments in exchange for goods or services

- A merchant bank, also known as acquiring bank, establishes and maintains merchant accounts. Merchant banks allow merchants to accept deposits from credit and debit card payments.

- The payment gateway The Payment Gateway sits between the Merchant and the Processor, who passes transactions to the card network (MasterCard, Visa, American Express, Discover, etc). The role of the payment gateway is that of a secure information conduit that complies with credit card processing security rules and regulations.

- A payment processor is an intermediary that enables transactions to flow through the system to obtain authorizations and deposits via the card network. Some financial institutions can be both the merchant/acquiring bank and the processor. In most cases, Merchants do not choose their Processor. It is usually determined as a result of which bank or financial institution your bank or Merchant Provider represents; however, this is transparent to you.

- Issuing banks are the banks, credit unions, and other financial institutions that issue debit and credit cards to cardholders through the card network. The issuing banks are responsible for approving or declining transactions and are committed to making payments on behalf of the customer/cardholder.

- Card network includes Visa, Mastercard, Discover, and American Express. The card network sets interchange rates and qualification guidelines, and acts as an intermediary between issuing banks and acquiring banks.

A card network can function in different ways, depending on how it’s set up. If the card network is both the card network and the card issuer, the network will both process and approve purchase requests. This is how it works for American Express and Discover cards.

If the card network is different from the card issuer, the credit card network (Visa and Mastercard) acts as an intermediary that connects the merchant with the issuing bank to process and approve credit card transactions.

Two Stages of Transaction Processing – Authorization & Clearing/Settlement

1) Authorization

- Card details and purchase amount must first be verified and approved by the issuing bank. Authorization is the process by which the issuing bank approves or declines a card transaction. This takes place within a matter of seconds at the time of purchase.

- The issuing bank checks the validity of the credit or debit card used by the customer. This is done by utilizing various fraud prevention tools, including Address Verification Service (AVS) and Card Security Codes (CVV2, CVC 2 and CID).

- The response is received by the merchant.

2) Clearing and Settlement

- Clearing is a process through which an issuing bank exchanges transaction information with a payment processor.

- Settlement is a process through which an issuing bank exchanges funds with a payment processor to complete a cleared transaction.

- Clearing and settlement occur simultaneously.

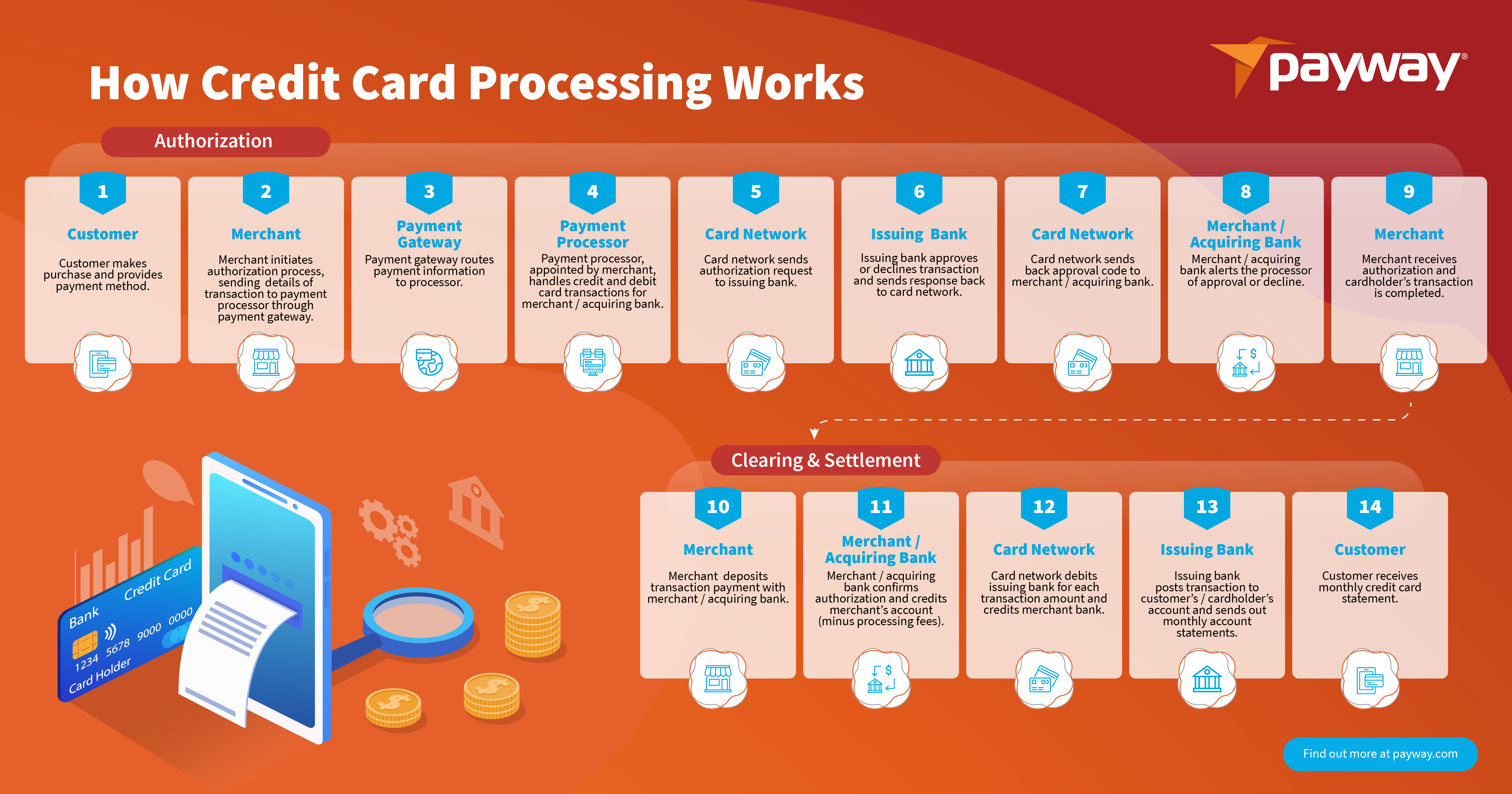

Authorization

1

The customer makes a purchase and provides a payment method. If a customer had placed the order online and is paying with a Visa credit card (a card network) provided by Chase (an issuing bank), there is no EMV chip or magstripe to swipe. Therefore, this transaction is processed as a card-not-present transaction and it is considered a higher risk transaction as the merchant cannot physically validate the credit card or the transaction. As a result, the interchange fee will be higher.

2

The merchant initiates the authorization process by sending the details of the transaction to the payment processor through the payment gateway. If the merchant works with a payment gateway that allows for level 3 processing (sends additional transaction information) the merchant qualifies for lower interchange rates.

3

The payment gateway routes the payment information to the processor. The moment card data is received via swipe, key, dip, or tap, the gateway securely transmits the payment information via the payment processor to the issuing bank for authorization.

4

The payment processor, appointed by a merchant, handles credit and debit card transactions for the merchant/acquiring bank. The payment processor routes the transaction information to the card network (Visa, Mastercard, etc.).

5

The card network sends an authorization request to the issuing bank.

Although the card networks don’t approve or decline a transaction, they need to know about it because they charge a fee (known as interchange fee) for every approved transaction.

6

The issuing bank approves or declines a transaction and sends back a response to the card network. The issuer also routes funds to the acquiring bank when a transaction receives approval. Assuming the cardholder has available credit and the account is active, funds are then sent from the issuing bank to the acquiring bank.

7

The card network sends back an approval code to the merchant/acquiring bank.

8

The merchant/acquiring bank alerts the processor of the approval or decline. If approved, money from the transaction (minus any fees and service charges) is placed into the merchant’s account.

9

The merchant receives authorization and the cardholder’s transaction is completed.

Clearing & Settlement

10

The merchant deposits the transaction payment with merchant/acquiring bank. A merchant will usually do this via a batch of authorizations to the acquiring bank at the end of each business day.

11

The merchant/acquiring bank confirms the authorization and credits the merchant’s account (minus processing fees). The merchant bank submits the transaction information to the card network for settlement.

12

The card network debits the issuing bank for each transaction amount and credits the merchant bank.

13

The issuing bank posts the transaction to the customer’s/cardholder’s account and sends out monthly account statements. A customer may see a charge go from “pending” to “posted” when checking their spending activity. This is because it usually takes one to three business days for the merchant to clear & settle transactions with other parties.

14

Customer receives a monthly credit card statement.