Account Takeover Fraud in Subscription Payments

Account takeover (ATO) has emerged as the fastest-growing and most damaging form of fraud for subscription-based businesses. Instead of stealing card numbers and testing them externally, attackers now focus on gaining access to customer accounts where:

• Payment credentials are already stored

• Trust is already established

• Fraud can occur without triggering traditional alerts

This shift is driven by a broader transformation in fraud behavior:

• Card-not-present (CNP) transactions now account for over 70% of global card fraud losses, exceeding $48 billion in projected losses for 2026 [wiserreview.com]

• Account takeover fraud specifically increased 37% year-over-year, reflecting a rapid shift toward identity-based attacks [clearlypayments.com]

The implication is clear: payments are no longer the primary entry point—accounts are.

What is Account Takeover Fraud, and Why Should Subscription Businesses Care?

ATO fraud occurs when criminals gain unauthorized access to legitimate customer accounts and use stored payment credentials to commit fraud. Because attackers operate within trusted accounts, ATO is often more difficult to detect than traditional card fraud. Subscription businesses can reduce risk by implementing multi-factor authentication (MFA), behavioral analytics, device fingerprinting, secure account recovery processes, and real-time monitoring.

Why Subscription Businesses Are Prime Targets for Account Takeover?

Subscription businesses are vulnerable because they store payment credentials, rely on recurring billing, and allow ongoing account access, making compromised accounts highly valuable to attackers. Subscription models create a perfect environment for ATO fraud.

1. Stored Payment Credentials

Once inside an account, attackers gain immediate access to:

• Saved credit cards

• Billing details

• Payment history

No need to validate stolen data—monetization is instant.

2. Recurring Revenue Streams

Unlike one-time fraud, ATO enables:

• Multiple transactions

• Ongoing billing abuse

• Subscription upgrades

Fraud becomes persistent, not transactional.

3. Trusted Customer Profiles

Compromised accounts often appear legitimate:

• Known email

• Established device history

• Existing billing patterns

This allows attackers to bypass traditional fraud detection.

4. Low Visibility Fraud

ATO fraud is often:

• Small in value

• Distributed over time

• Hidden within normal activity

Which makes it harder to detect than card fraud.

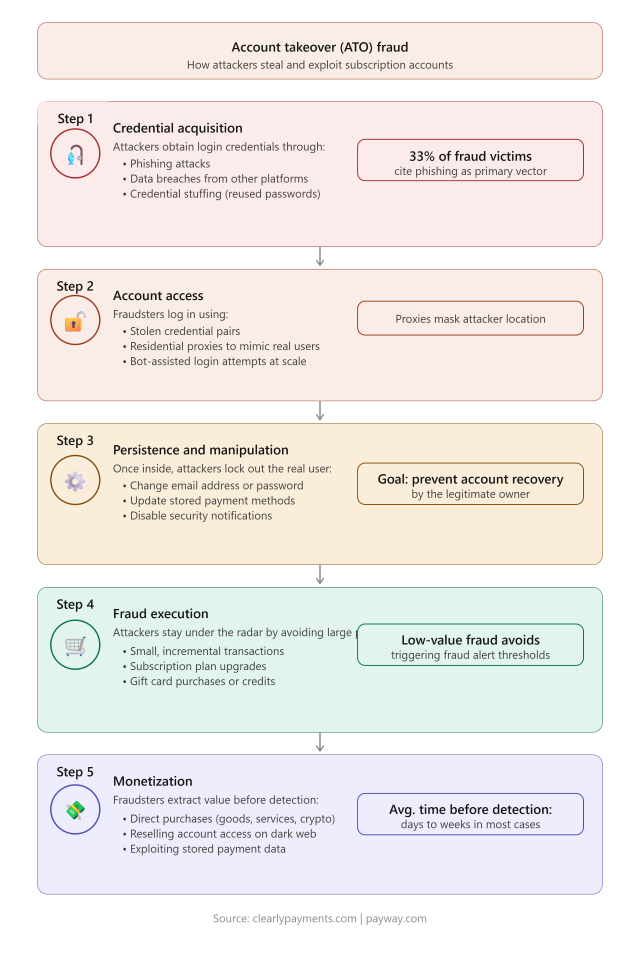

How Account Takeover Works

ATO attacks have become significantly more sophisticated due to AI and automation.

Step 1: Credential Acquisition

Attackers obtain login credentials through:

• Phishing attacks

• Data breaches

• Credential stuffing

Notably:

• 33% of fraud victims report phishing as the primary attack vector [clearlypayments.com]

Step 2: Account Access

Fraudsters log in using:

• Compromised credentials

• Residential proxies to mimic real users

• Bot-assisted login attempts

Step 3: Persistence and Manipulation

Once inside, attackers may:

• Change email or password

• Update payment methods

• Disable notifications

Step 4: Fraud Execution

Instead of large purchases, attackers use:

• Small transactions

• Incremental spending

• Subscription upgrades

This avoids triggering fraud alerts.

Step 5: Monetization

Fraudsters extract value by:

• Making purchases

• Reselling access

• Leveraging stored payment data

Warning Signs of Account Takeover

What are signs of account takeover fraud?

Signs include unusual login behavior, sudden account changes, new devices, multiple small transactions, and changes to payment or billing information.

Key indicators to watch:

• Unusual login locations or devices

• Spike in password reset requests

• Changes to account details

• Multiple low-value transactions

• Sudden usage pattern changes

The Business Impact of ATO

Account takeover is not just a fraud problem—it is a business risk multiplier.

1. Revenue Loss

Losses include:

• Fraudulent transactions

• Subscription misuse

• Refunds and disputes

2. Chargebacks and Liability

ATO fraud often results in:

• Chargebacks classified as unauthorized

• Increased dispute rates

3. Customer Trust Damage

Compromised accounts lead to:

• Loss of customer confidence

• Increased churn

• Negative brand perception

4. Operational Costs

ATO increases:

• Support volume

• Fraud investigation costs

• Security investment requirements

5. Regulatory and Compliance Risk

With stricter regulations (PCI DSS 4.0), businesses must:

• Protect account access

• Implement stronger authentication controls

Failure to do so increases liability exposure.

Why Traditional Fraud Detection Fails Against ATO

Most fraud systems were designed to detect transaction anomalies.

ATO exploits identity trust, not payment anomalies. Key gaps include:

Static Rules based on:

• Transaction size

• Geographic location

These are easily bypassed by attackers.

Lack of Behavioral Intelligence

Without behavior analysis:

• Legitimate-looking fraud goes undetected

• Session-based attacks are missed

Weak Authentication

Password-only systems are:

• Vulnerable to credential reuse

• Easily compromised

In 2026, these limitations make traditional systems insufficient.

How to Prevent Account Takeover

ATO prevention requires a multi-layered identity security approach.

✅ 1. Multi-Factor Authentication (MFA)

MFA is now a baseline requirement:

• Protects against credential theft

• Adds identity verification

Phishing-resistant MFA is recommended under modern identity standards.

________________________________________

✅ 2. Behavioral Analytics

Analyze:

• Login patterns

• Device behavior

• Session anomalies

Detects fraud even when credentials are valid.

________________________________________

✅ 3. Device Fingerprinting

Track:

• Known vs unknown devices

• Device consistency

• Risk scoring per device

________________________________________

✅ 4. Secure Account Recovery

Most ATO attacks exploit recovery flows.

Secure:

• Password reset processes

• Identity verification

• Support workflows

________________________________________

✅ 5. Real-Time Monitoring

Monitor:

• Account changes

• Payment updates

• Transaction anomalies

Respond instantly to suspicious activity.

________________________________________

✅ 6. Customer Education

Educate users on:

• Phishing awareness

• Password hygiene

• Account security practices

________________________________________

Advanced Strategy: Protect the Entire Identity Lifecycle

ATO prevention is not just login security—it’s lifecycle security.

Protect:

• Account creation

• Login

• Session activity

• Account changes

Fraud can occur at any step—not just login.

Final Thoughts

Account takeover is no longer a niche threat—it is the dominant fraud vector in subscription payments.

It represents a shift from:

• Transaction fraud → Identity fraud

• One-time attacks → Persistent exploitation

The businesses that succeed in 2026 will:

• Treat identity as part of payment security

• Invest in multi-layered defenses

• Detect fraud before transactions occur